Investment regulations and provisions on supervision not applicable to L‑QIF (CISA 118d)

The following provisions of the CISA are expressly not applicable to L‑QIF:

- The investment regulations of Art. 53–71 (for securities funds, real estate funds and other funds for traditional and alternative investments) and Art. 103 (for KmGK);

Non-applicable provisions that grant FINMA a case-by-case competence or supervisory competence:

- 7/4/sentence 2: no exemption from the supervisory duty for the only investor of a single-investor fund who makes the investment decisions;

- 10/5: no exemption from regulations for funds for qualified investors;

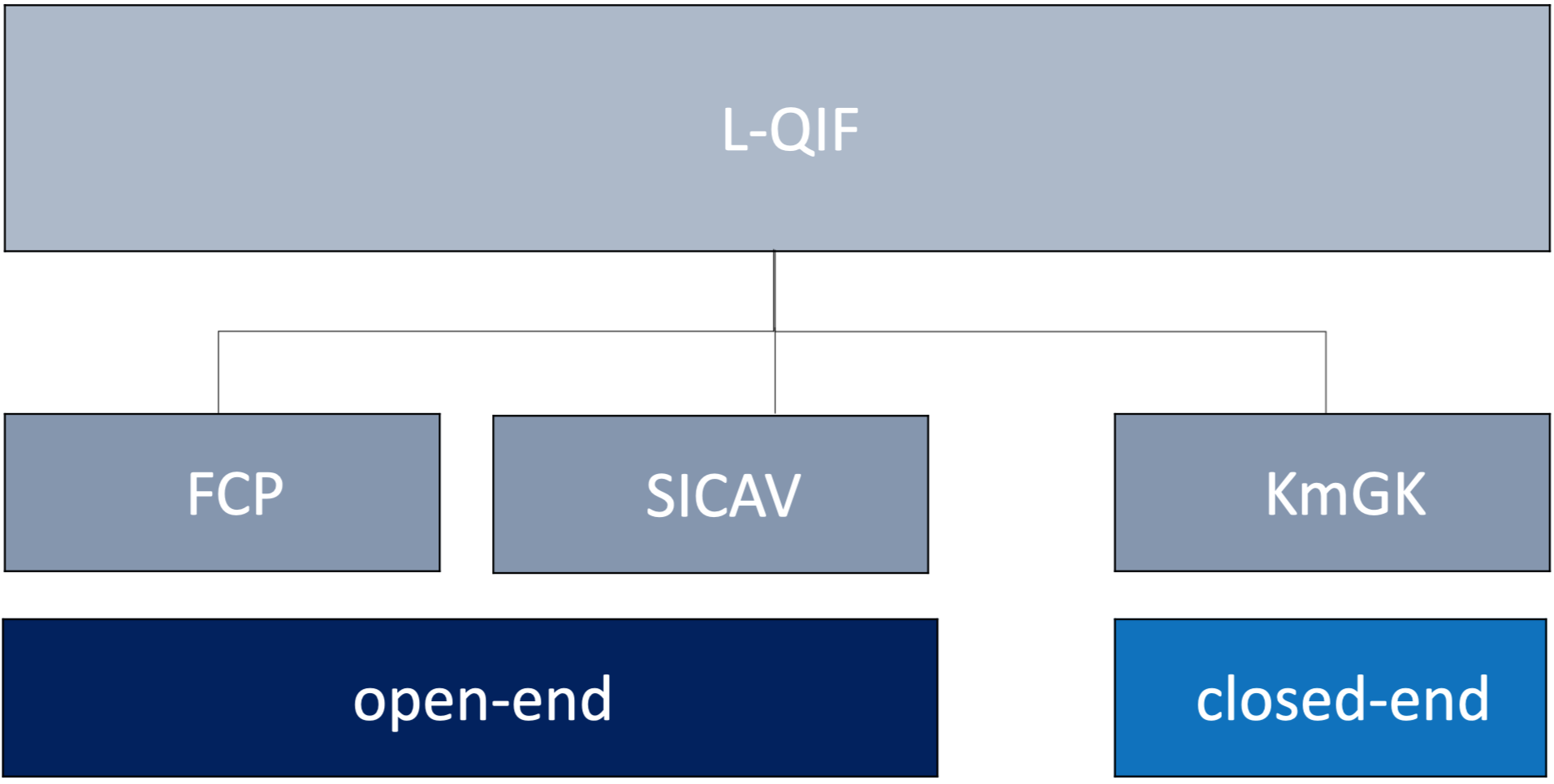

- 26/1 and 27: no approval of the fund contract and its amendments. Art. 15/3 CISA also expressly mentions that the fund documents of an L‑QIF do not require approval, and Art. 13/2bis now explicitly states that an L‑QIF in the form of a SICAV or KmGK does not require authorization;

- 39/2: no simplifications or tightening of the equity capital of the SICAV;

- 44a/2: no exceptions to the obligation of the SICAV to appoint a custodian bank;

- 47/2 (i.V.m. CISO 62/3): no order for the splitting or consolidation of shares of a share category in the SICAV;

- 74: no approval for custodian bank changes – see CISA 118k as lex specialis;

- 78/4: no approval of contributions in kind or distributions of assets in kind – see CISA 118l as lex specialis;

- 81/2: no granting of a postponement for the redemption of units – see CISA 118m as lex specialis;

- 83/3: no approval of deviating NAV calculation methods;

- 89/4: submission of annual and semi-annual reports to FINMA;

- 91: Regulations of the CISO-FINMA on accounting, valuation, reporting and publication requirements (Art. 79–108 CISO-FINMA) – see however CISA 118i as lex specialis;

- 95/2: no approval of restructurings;

- 96/1/c, 96/2/c, 96/4 and 109/c: no involvement of FINMA in the liquidation of the collective investment scheme;

- 126: no supervisory audit;

- 132–134 and 136–144: no supervision, supervisory instruments, compulsory liquidation or bankruptcy proceedings. CISA 132/3 also newly stipulates that an L‑QIF is not subject to the supervision of FINMA.

- 144: No data collection by FINMA (but probably by the FDF, cf. CISA 118f/5).

Where FINMA can approve a simplification for the collective investment schemes it supervises, the L‑QIFs are often subject to a stricter regime as a result. This is particularly annoying in the case of single-investor L-QIFs, where the investment decisions can only be delegated back to the single investor if the latter is supervised (cf. CISA 7/4/sentence 2 i.V.m. CISA 118d).

Information of investors and designation of the L‑QIF (CISA 118e)

The first page of the fund documents and the advertising must contain the designation “Limited Qualified Investor Fund” or “L‑QIF” and the indication that the L‑QIF is neither authorized nor approved nor supervised by FINMA.

In the case of the SICAV and the KmGK, the company must also contain the designation “Limited Qualified Investor Fund” or “L‑QIF” in addition to the designation of the legal form, i.e. e.g. “AVELA Fund 1, L‑QIF SICAV”.

It is prohibited to designate an L‑QIF as a “securities fund”, “real estate fund”, “other fund for traditional investments” or “other fund for alternative investments”. These designations are reserved for collective investment schemes to which certain investment regulations are assigned, which according to CISA 118d are expressly not applicable to an L‑QIF. However, only the listed terms are explicitly excluded. A designation such as “L‑QIF for real estate investments” or “Alternative L‑QIF”, on the other hand, should in our opinion be permissible if the name is consistent with the investment policy.

For the practitioner, it should be added that intentional violations of CISA 118e can be punished with a fine of up to CHF 500,000 (CISA 149/1/g).

For the protection of designations, compare also CISA 12/2, which was supplemented by the designations “Limited Qualified Investor Fund” and “L‑QIF”.

Reporting obligation and data collection (CISA 118f)

The institution responsible for the management of the L‑QIF, typically the fund management company, must notify the Swiss Federal Department of Finance (FDF) within 14 days if it takes over or relinquishes the management of an L‑QIF. The content of the notification will be regulated in the CISO. An intentional violation of this reporting obligation is also punishable (CISA 149/1/h).

The FDF maintains a public register of all L‑QIFs and the institutions responsible for their management and may collect (or have collected) statistical data. Despite the non-applicability of CISA 144 to the L‑QIF, CISA 144/2+3 concerning data secrecy now apply mutatis mutandis here.

Management of L‑QIF in the legal form of contractual investment funds (CISA 118g)

Analogous to the supervised contractual funds, contractual L‑QIFs are managed by a fund management company. The delegation of the investment decisions is governed by the provisions of the Financial Institutions Act (“FINIA”). Regardless of the volume of the L‑QIF, the investment decisions may only be delegated to a domestic or foreign manager of collective assets i.S.v. FINIA 24ff. (“CISA”). The de minimis rule of FINIA 24/2/a does not apply here: Anyone who is only authorized as an asset manager according to FINIA 17ff. may not act as a portfolio manager for an L‑QIF. However, the sub-delegation from a CISA to another CISA is possible. The delegation of the investment decisions to an authorization holder with a hierarchically higher authorization (bank, other fund management company) is also possible in our opinion. In our opinion, the provision should be read in such a way that the delegated portfolio manager must be authorized at least as a CISA.

The delegated portfolio manager must be named in the fund contract.

Management of L‑QIF in the legal form of SICAV and KmGK (CISA 118h)

An L‑QIF SICAV must transfer the administration and the investment decisions to the same fund management company. An L‑QIF in the form of a self-managed SICAV is therefore not possible; cf. Dispatch on the amendment of the CISA (“Dispatch”), p. 30.

An L‑QIF KmGK must transfer the management to a CISA, whereby this is again a minimum requirement. If the general partners (or, in our opinion, also the only general partner), i.e. the partners with unlimited liability, are banks, insurance companies according to ISA, securities firms, fund management companies or CISAs, the management does not have to be transferred.

The further transfer of the investment decisions is also governed in both cases by CISA 118g/2+3, i.e. is only permissible if the delegated portfolio manager is at least a CISA.

The L‑QIF must state in the articles of association (SICAV) or in the partnership agreement (KmGK) to whom the management or the administration is transferred. A change is therefore only possible by amending these documents in a qualified procedure. With regard to the amendment of the partnership agreement in the case of the KmGK in general, reference is made to Article 102a CISA, which was also newly inserted in the course of this revision.

Auditing, accounting, valuation and reporting (CISA 118i)

An audit firm licensed under the Audit Oversight Act must be entrusted with the audit of the L‑QIF, namely the same one as the institution which, according to CISA 118g or 118h, is responsible for the management of the L‑QIF. It is expressly stated that the L‑QIF bears the costs of the audit.

Detailed rules on this are to be expected at ordinance level (CISO). The Federal Council has been granted a fairly comprehensive competence to regulate accounting, valuation, reporting and publication requirements.

Creation and amendment of the fund contract for open-ended L‑QIF (CISA 118j)

In our opinion, the regulations concerning the fund contract of an L‑QIF do not differ significantly from the regulations for the supervised open-ended contractual investment funds or SICAVs, except that in the case of the L‑QIF, the approval by FINMA is omitted. The consent of the custodian bank must be obtained in any case, and in the event of amendments to the fund contract, the investors must be informed at least 30 days in advance and given the opportunity to redeem their units.

Change of custodian bank for open-ended L‑QIF (CISA 18k)

In the case of contractual investment funds, reference is made to the also new Art. 39a FINIA (“Change of the fund management company of a Limited Qualified Investor Fund”), which applies mutatis mutandis. Again, the procedure is similar to that up to now or as in the case of a normal fund contract amendment, and again the approval by FINMA is omitted.

Contributions in kind / distributions in kind (CISA 118l)

Contributions in kind or distributions in kind instead of payments or disbursements in cash are permitted for L‑QIFs of the open-ended type if they are provided for in the fund contract in the case of the contractual investment fund or in the investment regulations in the case of the SICAV. This provision replaces CISA 78/4, which was declared not applicable to the L‑QIF.

Postponement of redemption in extraordinary cases (CISA 118m)

In the case of an L‑QIF of the open-ended type (contractual investment fund or SICAV), the fund management company can autonomously order a temporary postponement of the redemption of the units in extraordinary cases in the interest of all investors. For the L‑QIF, this provision replaces Art. 81/2 CISA, according to which this competence lies with FINMA for supervised funds.

The idea that the right to return at any time for longer than a maximum of five years may be suspended for an open L-QIF has not been incorporated into the new version of the KAG. KAG 79/2 therefore remains applicable without change.

Investments and investment techniques (KAG 118n)

As mentioned, the KAG contains no regulations regarding permissible investments for the L-QIF. The investment regulations for supervised collective investment schemes of KAG 53–71 and 103 are declared inapplicable across the board (KAG 118d). Thus, all types of innovative asset classes seem to be possible even for open collective investment schemes, at least as long as adequate liquidity can be guaranteed, as is prescribed for the first time by a new provision (KAG 78a “Liquidity”), which also applies to supervised funds and SICAVs.

The only requirement is that the permissible investments must be regulated in the fund agreement, investment regulations, or articles of association. In the case of alternative investments, the special risks must also be pointed out, analogously to the “other funds for alternative investments” (KAG 71/3) known today in the designation, in the fund documents and in advertising.

Paragraph 3 does not seem entirely unproblematic to us, according to which the Federal Council is given the power to regulate investment techniques and investment restrictions in the Collective Investment Schemes Ordinance (KKV). We can look forward to the draft of the KKV with anticipation here. The industry should resolutely oppose any overly restrictive regulations.

Risk diversification (KAG 118o)

The provision only states that the risk diversification of an L-QIF must be described in the fund documents in accordance with KAG 118n/1, i.e. analogously to the permissible investments. It is certainly in the best interest of the providers of an L-QIF to ensure maximum transparency in these matters, on the one hand, in order to comply with the supervisory regulations, even if there is no prudential supervision, and on the other hand, in order to minimise the civil liability risk. According to the dispatch (p. 36), inadequate disclosure would not be permitted: “It must not simply be stated that the L-QIF is free in the risk diversification”.

Special regulations for real estate investments (KAG 118p)

This article regulates the special features if an L-QIF invests (exclusively or in addition to other investments) in real estate investments. The following regulations were taken from the world of supervised real estate funds:

- Liability of the fund management company for ensuring that the real estate companies belonging to the fund comply with the regulations (KAG 63/1);

- Prohibition of transactions with related parties (KAG 63/2+3), whereby the Federal Council has to regulate the exceptions in the KKV – compare KKV 32a for the supervised real estate funds;

- Appointment of independent valuation experts, whereby, in the case of the L-QIF, the mandate is not approved by FINMA as in the case of the supervised real estate fund (KAG 64/1+2).